Market Insights

Textile Industry in India

Overview

Textile Industry is one of the largest and oldest industries of the Indian economy that has undergone various developments throughout the years. The term textile refers to yarns, fibers and woven fabrics made from cotton, jute, wool, polyester etc. India’s first textile mill was established in Kolkata in 1818, however the Bombay Spinning and Weaving Company, which was established in 1854 laid the foundation for the modernised cotton industry in the country. The close connection of the industry with agriculture for raw materials and the ancient culture & traditions of the country makes it unique when compared to other industries. Being one of the key contributors to the economy, the textile industry in India has been recognised as one of the Sunrise Sector by the government.

The Textile Industry in India is segmented as,

- Fiber

- Yarn

- Fabric

- Apparels

- Home Textiles

- Technical Textiles

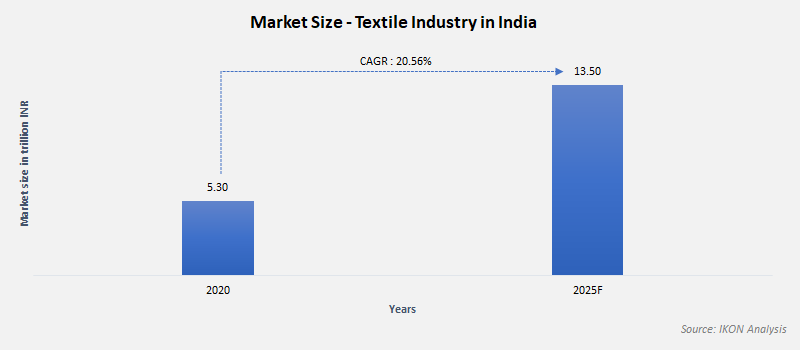

Textile Market Size in India

The Indian domestic textile and apparel industry contributed around 2.3% to the country’s overall GDP and was valued around 5.30 trillion in 2020 and the demand is expected to increase at a CAGR of 20.56% reaching INR 13.50 trillion by 2025.

In terms of production volume, cloth (excluding Khadi, Wool and Silk) makes up a major portion of the market with 89% which is followed by Cotton yarn with 5%. Other textile products contribute to less than 5% of the total market.

Competitive Landscape

The Indian textile industry is fragmented with most of the players operating in the unorganized market. The organised market is made by some well known companies such as; Welspun - India’s leading company in the Home Textiles segment whose net revenue stood at INR 59.5 billion in 2020-21. Followed by Vardhman, the company which specialises in Yarn whose revenue in 2020-21 was around INR 57.8 billion. While, Arvind the country’s major player in Fabrics & Apparel segment made a revenue of INR 45.28 billion in 2020-21. Other notable players are; Alok Industries, Sutlej, Raymond, KPR Mills, Nahar and Grasim Industries to name a few.

Growth Drivers for Indian Textile Industry

Favourable Government Initiatives & Policy

- Amended Technology Upgradation Fund Scheme was introduced by the Ministry of Textiles to facilitate investment, quality, productivity and employment for manufacturers.

- The government of India allowed 100% FDI policy through automatic route.

- Sustainable and Accelerated Adoption of Efficient Textile technologies to Help small Industries (SAATHI) scheme was launched majorly to improve the technology of the powerloom sector in India.

- Scheme for Capacity Building in Textiles Sector (SCBTS) was introduced to create jobs for youth in the textile sector by providing them with necessary skill development programmes.

Organised Retail Stores

India has become a very attractive market for international brands and many entered into the indian market in recent times. The presence of top international brands may push the demand for fashion apparel.

Technical Fabrics

Although at the nascent stage in India, technical fabrics have the potential to grow in the future due to the benefits it offers in various fields such as healthcare, automotive, construction, environmental protection, sports & fitness etc. for the domestic market.

Growing Population

India‘s population is expected to grow at a rate of 26% reaching 1.52 billion by 2026 and this might further increase the demand for textiles & apparels in the domestic market.

Challenges for Indian Textile Industry

Increasing Price of Raw Materials

Increasing raw materials cost poses one of the major challenges for indian textile manufacturers. The price increase of raw materials affects the operational cost and increases the price of end-product. Small and Medium Enterprises are majorly impacted due to the surge in price of raw materials.

Apparel Exports

Indian apparel manufacturers face huge price competition from emerging countries such as Bangladesh, Vietnam and Thailand for exporting textiles. Also factors such as reduced export incentives, time taken by the industry to adjust to new goods and service tax regime and credit crunch particularly with small and medium enterprises have negative effects on total textile exports of the country.

Inadequate Infrastructure

Lack of infrastructure, especially road networks poses a major challenge for the industry. India’s fashion industry is plagued by poor roads, highways and other infrastructure conditions creating supply chain constraints which in turn increases the lead time and warehousing costs.

Impact of Covid-19 on Indian Textile Industry

Indian textile industry is one of the most important sectors for the country’s economy in terms of output, employment and foreign exchange earnings. Due to the Covid19 pandemic the country implemented a nation wide lockdown which led to the closure of factories and lay-offs of employees. The local demand, export and import of textiles & apparels were reported nil during the lockdown period in 2020. According to the Confederation of Textile Industries, the export of textiles and apparels declined by 46.40% between April and July, 2020 when compared to the corresponding period of the previous year.

Future Outlook

The Covid19 pandemic has caused serious damages to the textile industry in India by ceasing operation for nearly three to four months. This resulted in a huge loss for the industry. It is expected that the Technical Textile segment will be a major driver for the textile industry. The National Technical Textile Mission aims at increasing the demand to approximately INR 2 trillion by 2024. Though it was expected that the textile industry will show signs of recovery in the second half of 2021, however, we estimate that the second wave of the coronavirus in India may push the textile industry recovery period to 2022.