Market Insights

Real Estate Industry in India

Overview

In 2020, India’s population stood at 1.38 billion and is expected to surpass China by 2030. The country’s economic transformation over the past decades has made it a potential business environment particularly in the service sector. Strong economic growth and favourable demographics has made India an attractive destination for real estate investors across the country. The Real estate sector is the second largest employer in the country. Real estate industry was historically an unorganized sector with absence of centralized title registry, lack of transparency in transaction, unavailability of financing etc. In recent times, the real estate sector is evolving towards a well regulated and transparent business environment that helps the long term growth of the industry.

The Real Estate Industry in India is segmented as;

- Residential

- Commercial

- Retail

- Hospitality

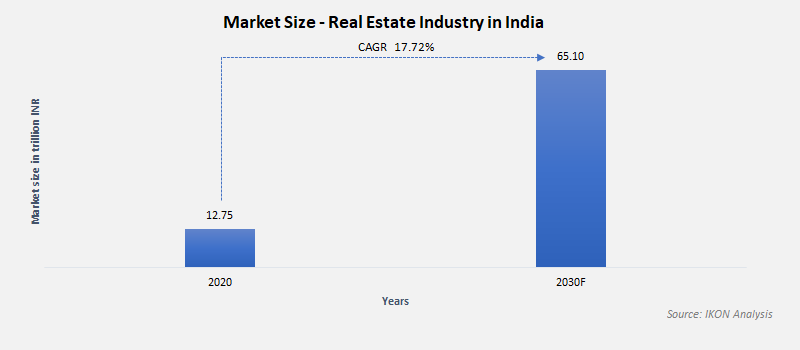

Real Estate Market Size in India

The real estate industry in India is expected to reach INR 65.10 trillion by 2030 from INR 12.75 trillion in 2020. The Industry is expected to grow at a CAGR of 17.72% between 2020 and 2030.

Competitive Landscape

Although the real estate industry in India is becoming more regulated over the past few years, the major portion of the space is occupied by unorganised players. However, some of the major players contributing to the organised market are; Macrotech Developers or most popularly known as the Lodha Group dominates the organised market witnessing a revenue of INR 42.9 billion in 2020-21. Followed by Prestige Estates Projects with revenue of INR 40.5 billion in the same year. While India's oldest real estate developer DLF clocked a revenue of INR 28.9 billion in 2020-21 and in the same financial year Sobha builders witnessed INR 20.9 billion as revenue. Other players include IndiaBulls, Godrej Properties, Oberoi Realty, Jaypee Infratech and Unitech.

Growth Drivers for Indian Real Estate Industry

Favourable Government Initiatives & Policy

- The Government of India launched Pradhan Mantri Awas Yojana to provide affordable housing to all lower and economically weaker sections of the society.

- Real Estate Regulation & Development Act (RERA) was introduced in 2016 to bring transparency in transaction with in industry and to protect the interest of consumers.

- Smart City Mission initiative was launched to develop and improve the quality of people by tapping into the latest technology and smart solutions.

- Real Estate Invest Trust was established to allow safe investments in the real estate sector in the country.

Increase in Disposable Income

The demand in the real estate industry in India is majorly driven by the rising disposable income of the people. As their income increases they are able to spend more, especially on residential housing.

Growth of Information Technology sector

The growth of the IT and ITES sector has fueled the industry generating demand for commercial buildings. These companies are setting up world class & highly integrated business centers to accommodate their growing labour force. As this sector is estimated to grow further, commercial segments are expected to become a major revenue driver for the real estate industry.

Organised Retail

The organised retail category is expected to grow by 22% in 2021 and further in the upcoming years. The growth is primarily driven by changes in shopping habits, rising income level, entry of foreign players and increasing number of retail malls. These factors will further push the demand in the real estate industry.

Challenges for Indian Real Estate Industry

Litigated Land

One of the major challenges for real estate developers is litigated lands. Data from 2019 reveals that, approximately 16% of the projects and 31% of built-up spaces are and have been in legal disputes in India. Due to this, projects are struck for a prolonged period of time.

Obsolete Building Technique

Indian real estate developers are still clinging to old construction techniques and dependent on a large human workforce. These techniques require regular maintenance. It is pivotal that developers should transition to new methods of construction so that they reduce the dependency on human labour and ensure faster deliveries.

Delayed Infrastructure Projects

Indian real estate market is clogged with long-delayed projects because of uneven / irregular funding and lack of latest construction technologies. Because of the absence of single-window clearance, project approvals take a longer time in India.

Impact of Covid-19 on Indian Real Estate Industry

The real estate industry in India was worst hit by the coronavirus outbreak in 2020. India went into a complete shutdown between May and June and this halted the entire property transaction. The lockdown has caused the labourers to migrate to their villages and this completely stopped the construction of housing projects across the country. The covid crisis has led to the shortage of raw materials such as cements, tiles, bricks, switches etc due to the supply chain disruptions caused by factory closures. It was estimated that the residential sales were down by 29% and a 30% decrease in office net absorption with 8.2 million sq. feet leased in Q1 of 2020 when compared to Q1 of 2019. Around 250 small and medium businesses related to real estate such as steel bars, aluminium panels, construction machinery parts reported huge losses in 2020 along with increase in operating costs, which further hindered the sales. However, NRI investments are a ray of hope for the real estate sector. A decrease in deposit rates in the range of 6-7% and the decline of Indian rupee against US dollar encouraged more NRIs to invest in real estates during the covid crisis.

Future Outlook

The Covid19 pandemic has caused unimaginable damage to all aspects of the Indian economy and the real estate sector is not an exception. The Indian government’s significant spending on infrastructure projects resulted in a growth of 14.5% in Q4 of 2020 Y-O-Y in the construction sector. However, the second wave of the coronavirus has paused the growth of the industry temporarily. With the falling mortgage rates, demand for affordable housing may increase significantly in the upcoming days. Also, it is estimated that the ready-to-move properties will be the preferred choice for customers in the post-covid era. The real estate sector had dealt with so many challenges before including the global financial crisis of 2008 and NBFC crisis of 2018 and has emerged stronger every time. We are optimistic that the real estate sector may recover by Q3 of 2021.