Market Insights

Automobile Industry in India

Overview

The automobile industry can be identified as the mother of all the manufacturing industries of a country since this has a direct impact on other related industries such as Iron and Steel, glass, rubber, plastic, chemical, logistics, banking, insurance, and ofcourse petroleum. The Automobile Industry in India is considered to be one of the most important macroeconomic growth drivers of the country. Indian automobile industry emerged as the 4th largest in the world in 2019 replacing Germany and expected to become the third-largest market in 2026 in terms of volume. India remained the world’s largest manufacturer of two-wheelers and tractors.

Automobile Market Size in India

Gasoline Vehicles

The automobiles generally consist of Gasoline Vehicles and Electric vehicles, the later being the focusing on usage of clean energy rather than depending on the oil. The automobile market in India was valued at approx INR 8,260 billion in FY 2018-19, which accounted for 7.1% of the total GDP of the country, 27% of the Industrial GDP, and 49% of the Manufacturing GDP. The automobile manufacturing industry includes the production of 2-wheelers, 3-wheelers, passenger vehicles and commercial vehicles. The total sales of automobiles increased at a CAGR of 9.61% from FY16-17 till FY18-19. However the total sales of vehicles fell by 13.62% in 2020-21 when compared to the previous year, mainly due to covid-19 lockdown implemented in the country.

Automobile industry in India is primarily dominated by Two-wheelers and Passenger Vehicles. In FY20-21 two-wheelers accounted for 81% of the overall market share while passenger cars accounted for 15% with a combined total sales of 17.82 million vehicles.

Electric Vehicles

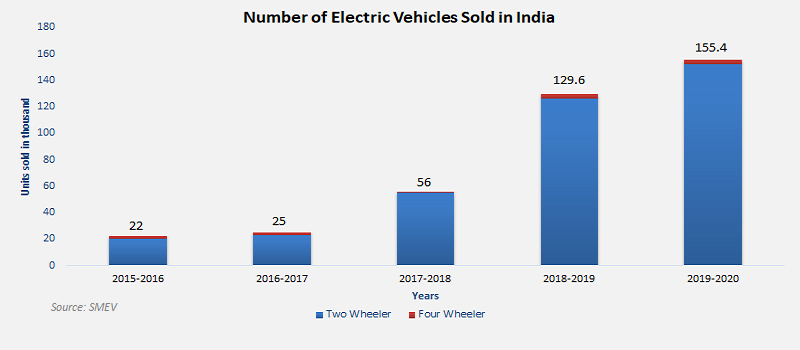

The Electric Vehicle market in India is growing consistently over the years.The sales of Electric Two-Wheelers has witnessed a growth at a CAGR of 66% between FY15-16 and FY19-20 with over 150,000 vehicles sold in FY19-20. While the Electric Four-Wheeler segment has grown with a CAGR of 14% from FY15-16 till FY19-20.

In FY19-20, Electric Two-Wheelers and Electric Four-wheelers accounted for 98% and 2% respectively with a combined sales volume of 155,000 vehicles. According to IESA, the EV market is forecasted to grow at a CAGR of 36% till 2026.

Market share of leading automobile players

Two Wheeler

The Indian automobile industry is primarily made of two-wheeler segments and Hero Motocorp & Scooter India Pvt Ltd and TVS Motor Company Ltd accounts for 26% and 15% respectively. Other manufacturers including EVs hold a market share of 8%. dominates the two-wheeler segment, holding 36% of the total market share.

Passenger Vehicle

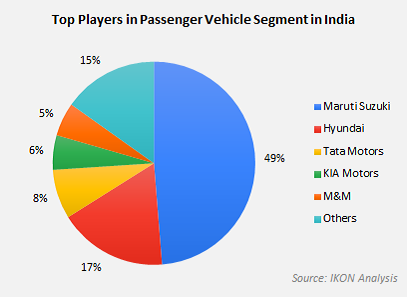

Maruti Suzuki is the leader by holding a major market share, 49% in the passenger vehicles segment. Hyundai Motors holds 17% of the total market share and TATA motors with 8%. While 15% of the market share is held by other manufacturers in the industry.

Commercial Vehicle

The Commercial Vehicles segment in India is dominated by Mahindra & Mahindra Limited holding 36% of the overall market share. TATA Motors comes in the second position holding 29% and Maruti Suzuki, a prominent player in the passenger vehicles segment, holds a minor share of 6% in the commercial vehicles segment.

Growth Drivers for the Indian automobile industry

According to the industry experts and automotive marketing consultants in India, the following factors will drive the growth of the industry in the years to come.

Favourable Government Initiatives & Policy

The automotive industry is the major contributor to the Indian economy and some of the initiatives introduced are;

- The Indian government has allowed a 100% FDI policy in the automotive sector to enable foreign companies to invest in the country

- Initiatives such as ‘Make in India’ and ‘Atmanirbhar Bharat Abhiyaan’ or self-reliant India were introduced by the Indian government to promote manufacturing within the country

- Automotive Mission Plan 2026 can be considered as one of the growth drivers as this vision aims to ensure universal mobility for every person in the country and also to increase the exports of locally manufactured vehicle

- The FAME India scheme encourages auto manufacturers to produce electric vehicles in India by subsidizing the production cost

- Vehicle scrappage policy ensures no vehicle can be on the road post 15 year period from the date of purchase

Preference for Private Vehicle

After the coronavirus pandemic, people prefer to commute in their vehicle rather than using public transport and other modes of transportation. This has created a new demand for automobiles in the country.

Technological Development

India, alternatively called the next Silicon Valley, is continuously prospering in advanced technologies from Robotics to Mechatronics, Artificial Intelligence, and Data Mining. These technological advancements are shaping the future of the automobile industry and since India is consistently updating to the latest technology this can boost the growth of the industry.

Growing Middle-Class Population

India, being the second-most populous country in the world, the country’s economy is majorly driven by people in the middle-class, and by 2030 around 140 million people will enter into the middle-class category which may increase the demand for automobiles.

Migration to Suburbs

The coronavirus pandemic has forced people to exit the city and move into the suburbs where limited public transportation is available and this may increase the demand for an automobile.

Challenges for the Indian Automobile Industry

Affordability towards Electric Vehicles

Although the government’s push for electrifying vehicles is on the rise, the cost of production is high when compared to gasoline-powered cars, thus affordability of the people in the country remains still debatable.

Change in Customer Preferences

In recent times there is a shift in customer preference from compact SUVs to connected cars and also due to the increased competition within the industry automakers find it difficult to satisfy their needs.

High Tax Rates

Luxury carmakers in India attract high tax rates between 48% and 50%, which makes the premium auto manufacturers hard to sell their products since these taxes increase the overall price of the cars.

Impact of Covid-19 on Indian Automobile Industry

The Covid19 of 2020 caused havoc around the world and the Indian automobile industry suffered heavy losses of INR 2,300 crores per day during the covid-19 lockdown period in 2020. Due to the pandemic situation, it is estimated that, the sales volume of two-wheelers may decline between 16% and 18%, while the volume of passenger vehicles sales may reduce by 22% to 25%, and light commercial vehicles sales volume may drop by 17% to 20% and a sales volume drop of 35% to 40% may be noticed in the medium and heavy commercial vehicles segment.

According to ACMA (Automotive Component Manufacturers Association of India), customer traffic at the physical showrooms has declined by 70% to 80% due to covid19 restrictions and this might bring down the sales of automobiles for a short period.

Future Outlook

The Indian automobile industry is expected to become the third largest in the world by 2026 with a market value of over USD 300 billion. However, semiconductor shortages and increasing raw material prices still pose a threat in the supply chain due to the closure of factories and country wide lockdown in 2020. According to IKON’s estimates, because of the ongoing second wave of the coronavirus pandemic, the sales of automobiles in India may decline further in the current fiscal 2021-22 and can expect a recovery beyond 2022.